As a foreigner in China, are you paying more tax since 2019 under new tax law asks Lily Li of Axel Standard

News of recent changes to Individual Income Tax (IIT) for foreigners in China spread like wildfire over WeChat and other social networks. Numerous amendments regarding the “five-year rule” fueled uncertainty as foreigners were left wondering whether the rule would remain or not. Effective January 1st, 2019, the five-year rule not only remains but has been increased to six years, amongst other changes to IIT law for foreigners in China.

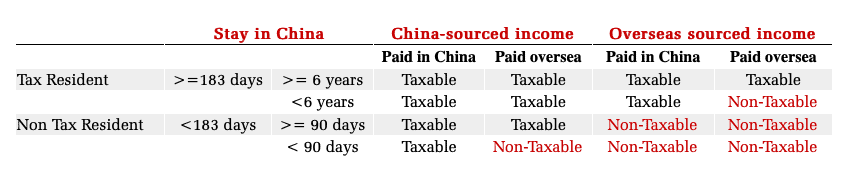

China new IIT Law: Tax Resident and Non-Tax Resident

China’s new IIT law, which took effect from January 1st, 2019 defines tax / non-tax residents in line with OECD tax guidelines. Foreigners, including HK, Macau and Taiwan passport holders, who reside in China for a cumulative total of 183 days or longer within a tax year – which runs from January 1st until Dec 31st – are considered a “Tax Resident” and will be taxed on their worldwide income. Anyone residing in China for less than 183 days over a tax year will be considered “Non-Tax Resident” and taxed only on the China-sourced income.

Tax Resident: The five-year rule becomes the six-year rule

Under old IIT law, the five-year rule stated that income sourced and paid overseas is exempt from China individual income tax for five years, after which it will become taxable in China. A well-known tax concession within IIT law has allowed countless foreigners living in China to extend the five-year tax exemption period repeatedly. This has been possible, because – under the previous system – if a foreigner should leave China for more than 30 days consecutively or 90 days cumulatively in any tax year during a five-year period, they “reset” the clock on the five-year tax exemption period.

Under the new IIT Law, the five-year tax exemption period has been increased to six years, and if the foreigner leaves China for more than 30 days consecutively in any tax year during a six-year period, they “reset” the clock on the tax exemption period, and the income sourced and paid overseas is exempt from China’s Individual Income Tax.

Non-Tax Resident: 90-day rules

Included in the new IIT law effective January 1st, 2019, are the same tax exceptions for non-tax residents working in China. Foreigners who come to China to work for a period of fewer than 90 days cumulatively in a tax year can have their China-sourced income exempt from China individual income tax as long as the income is paid and borne overseas.

Below is a chart of how tax liability is recognised under the China New IIT Law

New filing requirements

The new IIT law also introduces comprehensive income tax filing. This replaced the special tax rates for remuneration of services, income from royalties and authors’ remuneration with the progressive income tax rate applied to wages and salary. China tax residents must now file provisional monthly tax return along with an annual tax reconciliation return between March 1st to June 30th of the following year based on the comprehensive income. Non-tax residents must file tax returns on a monthly basis or on each occurrence.

Effective January 1st, 2019, the five-year rule not only remains but has been increased to six years

Phasing out preferential tax policy

Since 1994, foreigners in China have enjoyed preferential tax policies in the form of non-taxable allowances (e.g. housing allowance, meal allowance, education allowance, home-country visits etc.) without an official ceiling amount. They often make up between 40 percent to 50 percent (or even higher) of compensation packages for foreigners living and working in China, thus allowing foreigners to significantly reduce their tax liability.

From January 1st, 2019 however these preferential tax policies will be transitioned out over a period of three years (ending on December 31st, 2021) and will be replaced with a single tax policy for both foreigners and locals. This single tax policy includes six itemised deductions based on standardised amounts.

** Old policy: No-cap deductions must be claimed using authentic Fapiaos (China official tax invoices) and relevant supporting documents. See FOCUS guide to Fapiao accounting here.

Starting on January 1st, 2019, foreigners working in China can choose whether they want to utilise the new itemised deduction policy or continue to enjoy the preferential tax policy currently provided to them until December 31st, 2021. If the foreigner chooses to change over to the new policy early, they will be unable to transition back to the old policy within a tax year.